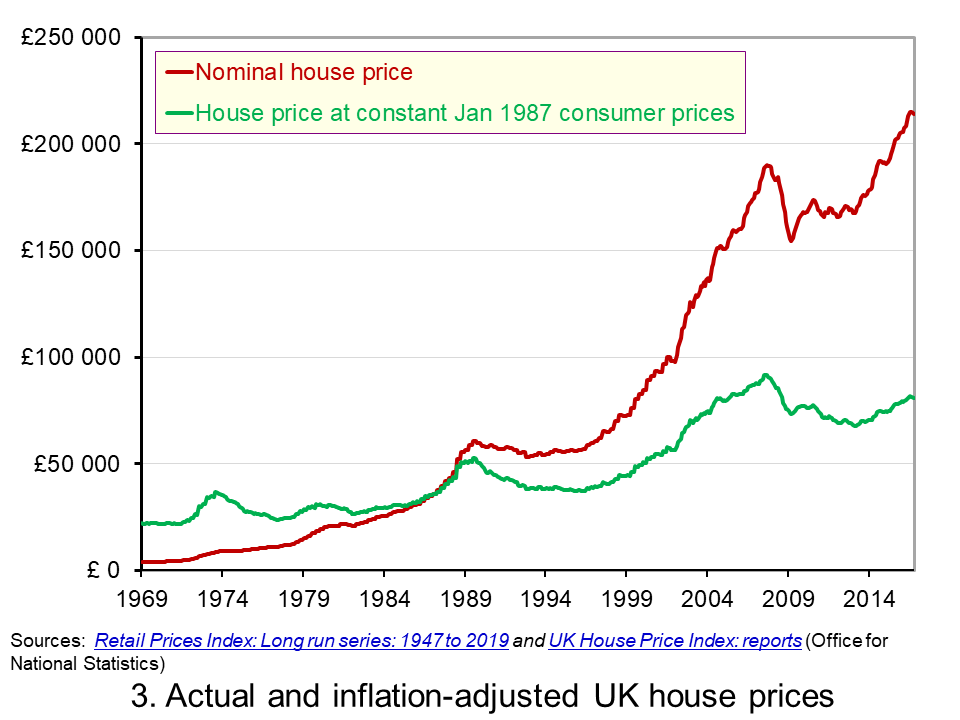

Housing barely appreciates above inflation. About 4% on average, yearly. It would be better if we didn't interfere in the market, or there are going to be some nasty consequences.

And yet housing has outpaced wages exponentially for decades - that's the appropriate comparison, not the stock market or inflation with a broader index.

Kiwi moved to the UK and housing market is just insane here, not even just London. Not only have house prices outpaces inflation (lack of new being built, housing being used as "investments" etc) but also stagnant wages.

The only reason I'll ever be able to afford a smallish house here is being on a tech salary; take average London wage here...and without generational wealth transfer they _cannot_ buy a house. Even with generational wealth transfer, our London salary friend will have to buy a house _outside_ london and commute (or wfh).

It's not a "hot market" it's just the haves have a vested interest in keeping the prices high for the have-nots. Just look at how landlords reacted to tenants getting some basic rights (that we've had in NZ for ages) "the sky is falling".

And all of this is for terraced houses at best, sharing a wall with neighbours, not detached at all, maybe you get a backyard maybe not. All made out of brick and built in the 40s-60s for the most part - and falling apart because of this. Never have I seen so much scaffolding since I moved to the UK.

There are still a few great things about living in the UK, but the housing market (amongst other things, wage gap, classism, corruption, population political apathy) is an absolute disgrace.

You're saying they're wrong that housing barely appreciates above inflation, around 4%, citing as an example a relative's sale of a house held for 50 years for 7.5x the real price.

Care to take a guess what 4% compounded for 50 years is? It's +611% or a total of 7.1x the original price. Your relative experienced 4.11% annual real gains, pretty close to 4%.

Over the last 70 years, a 300% gain in real terms is an annual increase of just 2%. That is barely outpacing inflation in my book.

> Over the last 70 years, a 300% gain in real terms is an annual increase of 2%. That is barely outpacing inflation in my book.

Your barely ain't my barely, that is for sure.

Compared to any other form of retail investment an average UK consumer could make instead (assuming they still also need to pay for accommodation), 2% over inflation consistently over that period is very significant. 4% over inflation is surely massive. (Particularly since the last 15 years of consumer savings yields have barely matched inflation, as I understand it; no matter, since the average consumer has not been able to save meaningfully since 2008 anyway).

As a store of consumer wealth in the UK, there is nothing even remotely close to housing.

There is an HN worldview distortion where buying a house is something really almost everyone here can hope for, and having the kind of resources and risk capacity to access opportunities with greater than 4% interest is not unusual.

In that same 70 year time period, the S&P 500 total return was 1234x against a USD inflation figure of 11.5x, for a real return of 107.3x or a real return CAGR of 6.9% versus the 2% CAGR that housing appreciated.

Surely, a UK investor can invest in the S&P 500 today. Go do the same math for the FSTE 100; I suspect it will also crush housing, just as the SP500 does in the US.

> There is an HN worldview distortion where buying a house is something really almost everyone here can hope for

In the US, ~2/3 of households own their homes, almost identical to the UK figures.

> Surely, a UK investor can invest in the S&P 500 today. Go do the same math for the FSTE 100; I suspect it will crush housing.

Yeah of course, after they have paid for their endlessly rising rent (because they aren't buying a house in this comparison, are they). And all their bills, and their food, and their energy.

Sorry: average UK people aren't investors, and nor are average Americans. This is the bias I am talking about. You're just not thinking the same way I am thinking. You are in a box where people have money to make investments.

> In the US, ~2/3 of households own their homes, almost identical to the UK figures.

Wrong way to look at it though. In the UK, the vast majority of people under 40 do not have a mortgage.

A majority of those people will never own a property. Even if their parents own a property, they are not particularly likely to inherit enough of a share of that money to secure a deposit on a house, because they are likely to have siblings and their parents are likely to have had to release equity to pay for their elderly care or pay bills.

Some but by no means most parents die with enough savings that an only child can inherit the house after all the taxes are paid; the average house price is very close to the IHT threshold.

The _average_ deposit in the UK is now 15%. That, combined with the fact that the average person in the UK is bearing down on 50 when they do inherit and will tend to need a higher deposit than a first time buyer...

4% above inflation is a dream.

I guess in the USA you still have little boxes being built on virgin hillsides. That is over in the UK; it's been over for 25 years. The limited supply of housing in the UK in the last 50 years will absolutely blow you away.

> Indeed, if someone spends everything they earn, they can neither invest nor save up a downpayment to buy a property.

This is, at a first approximation, everyone in the UK right now who does not already have a mortgage. A majority of people in the UK are spending more than they earn at the moment (for at least some months this year). And almost no mortgage holders are saving in anything other than employer pensions.

Just shy of 10% of UK mortgage holders will even have missed a mortgage payment at least once this year.

{kind=link}